7 Micro-Saving Hacks That Truly Work

Did you know that a 2025 survey found that most Nigerians admit that Inflation and high living costs make saving and budgeting difficult, with many people choosing not to track spending at all?

In Nigeria, your salary often disappears before the weekend. Between rising living costs, unexpected expenses, and the pressure of supporting family, saving money can feel like an impossible task.

Unfortunately, it’s easy to see why many Nigerians struggle to build a financial cushion. But here’s the ‘not-so-bad news’: you don’t need a large income to start saving. By adopting micro-saving habits and leveraging technology, you can begin building your savings, no matter how small your starting point.

In this article, we’ll explore micro-saving habits and a solution that makes savings for Nigerians a walk in the park.

Why Saving Feels So Hard in Nigeria

Saving in Nigeria presents unique challenges. According to a study by J. Abubakar (2025), financial shocks significantly impact the savings behavior of middle-class Nigerians, leading to reduced financial resilience. Some factors contributing to this include:

- High Cost of Living: Inflation and fluctuating prices make saving and budgeting difficult. According to the National Bureau of Statistics, Nigeria’s inflation is going up, which means everyday stuff is getting more expensive. In April 2025, it hit 22.22%, up from 21.91% in March. This drop in purchasing power makes it tougher to save money.

- Irregular Income: Many Nigerians experience inconsistent earnings, complicating saving efforts. If you’re freelancing, running a small business, or in the informal sector, your income can jump around a lot. This RSIS International study even shows that small businesses often struggle with inconsistent cash flow, which makes saving feel nearly impossible. Basically, you never quite know how much will hit your account each month.

- Black Tax: Then there’s the whole “black tax” thing. Helping family is a big deal here, and it can eat up a chunk of your income before you even think about saving for yourself. That’s why personal savings often take a back seat, even when you really want to build a safety net. The cultural expectation to support extended family members can strain finances.

- Emotional Spending: And let’s not forget how tempting life can be. Whether it’s catching up with friends, social media inspiration, or just wanting the latest gadget, it’s easy to spend impulsively. Research shows that financial literacy, especially budgeting can help manage this, but even small habits make a big difference.

These challenges can make saving seem daunting. However, adopting micro-saving techniques can help overcome these barriers.

The Power of Micro-Saving

Saving doesn’t have to be scary or complicated. In fact, the trick is in the small stuff. That’s where micro-saving comes in. Think of it like sneaking money into your piggy bank bit by bit—you barely notice it, but over time, it adds up big time.

Even research backs this up. A study in Abuja found that people who practiced micro-saving—setting aside tiny amounts regularly—saw their financial situation improve and were more confident handling money.

Here’s why it works so well:

- Small Steps Are Easier – Saving N1000 a day doesn’t feel like a sacrifice. Over a month, that’s N30,000; over a year, it’s N365,000. Not bad, right?

- Consistency Wins – The key isn’t dumping a huge chunk of cash at once; it’s doing it regularly. Automation helps a lot here.

- A Safety Net Without Stress – Over time, all these little deposits build a cushion you can actually rely on; perfect for emergencies, unexpected bills, or just peace of mind.

Basically, micro-saving makes it effortless to save. It’s like tricking yourself into being financially responsible without even realizing it.

7 Micro-Saving Hacks You Can Start This Week

- 100 Naira Daily Challenge

Commit to saving ₦1000 daily. While it may seem modest, this amounts to ₦30,000 monthly and ₦365,000 annually. Over time, this practice can significantly bolster your savings. - Save Windfall Income

Allocate a portion of unexpected income, such as bonuses or gifts, directly into savings. This approach prevents the temptation to spend windfalls impulsively. - 70/20/10 Rule

Adopt the 70/20/10 budgeting rule: allocate 70% of your income to expenses, 20% to savings, and 10% to discretionary spending. This framework promotes balanced financial management. - Black Tax Buffer

Set aside a specific amount each month for family support obligations. Treating this as a fixed expense helps prevent it from derailing your savings goals. - Save Your “Transport” Money on Remote Days

On days when you work from home and incur no transportation costs, transfer the saved amount into your savings account. This practice capitalizes on unspent funds. - Automate Savings

Utilize banking apps that allow for automatic transfers to your savings account. Automation ensures that saving becomes a non-negotiable habit.

How Moniger’s Savings Feature Makes It Easy

Moniger offers a user-friendly savings feature designed to simplify the savings process:

- Open the Moniger App: Navigate to the “Savings” tab.

- Set a Savings Goal: Define your target amount, such as an emergency fund.

- Enable Auto Top-up: Choose the frequency of automatic savings—daily, weekly, or monthly.

- Monitor Progress: Use the visual progress bar and streak tracking to stay motivated.

- Receive Notifications: Get alerts celebrating your milestones to reinforce positive saving behavior.

By integrating these features, Moniger helps you build and maintain effective saving habits.

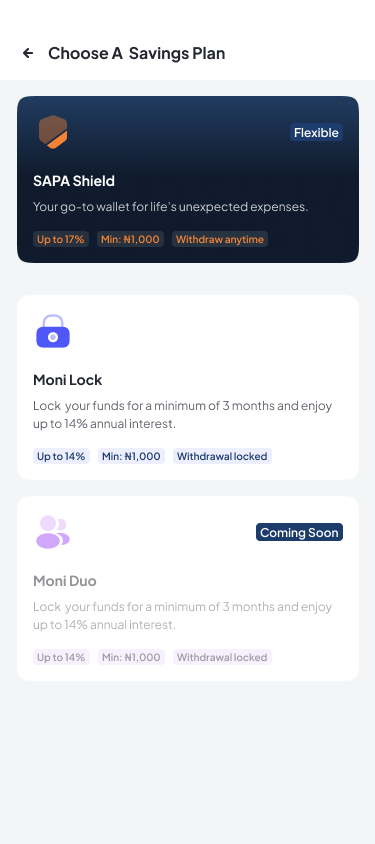

Meet Moniger’s Savings Plans: Sapa Shield, MoniLock, and MoniDuo

Saving isn’t one-size-fits-all. That’s why Moniger gives you three smart options to grow your money depending on your needs and goals.

1. Sapa Shield: Your Emergency Buddy

Think of Sapa Shield as your go-to wallet for life’s surprises. If you need a small cash buffer for an emergency, Sapa Shield has you covered. It’s flexible, you can withdraw anytime, and your money earns up to 17% interest per annum. Perfect for people who want high returns without locking themselves in.

2. MoniLock: Commit and Grow

If you’re serious about saving, MoniLock helps you lock your funds for a minimum of three months. In return, you earn up to 14% interest per year. The catch? It’s not flexible; you can’t withdraw early. But if you stick to your plan, your savings will grow faster. MoniLock is for when you have a goal and want to see your savings grow steadily. You can save for things like a house, a car, study, or travel, and your money earns up to 2.6% interest per month.

3. MoniDuo: Save Together

Saving is better with a partner. MoniDuo works just like MoniLock, but for two people. You can set joint goals, lock your funds for at least three months, and watch your savings grow together. It’s perfect for couples, friends, or business partners who want to save with accountability.

Tip: Choose Sapa Shield if you want flexibility, MoniLock if you want higher interest with discipline, and MoniDuo if you want to save with someone else.

How to Stay Consistent (Even When Income Is Irregular)

Maintaining consistency in saving, especially with irregular income, requires discipline and planning:

- Treat Savings as Fixed Expenses: Prioritize savings by allocating funds before other expenses.

- Track Progress: Use apps like Moniger to monitor your saving habits and celebrate achievements.

- Start Small: Begin with manageable amounts and gradually increase as your financial situation improves.

- Build Trust in the System: Rely on automated features to reduce the temptation to spend.

Start Building Your Safety Net Today

Building financial security doesn’t have to be complicated. It all starts with small, consistent steps. Use micro-saving hacks and tools like Moniger to slowly grow a cushion you can actually trust with peace of mind included.

Ready to get started? Download Moniger today and save your first N1000. You’ll thank yourself later.